Report on economic position

Economic environment

Macroeconomic environment

Subdued economic development

Both national and international economic development are crucial for a global air traffic hub such as Munich Airport.

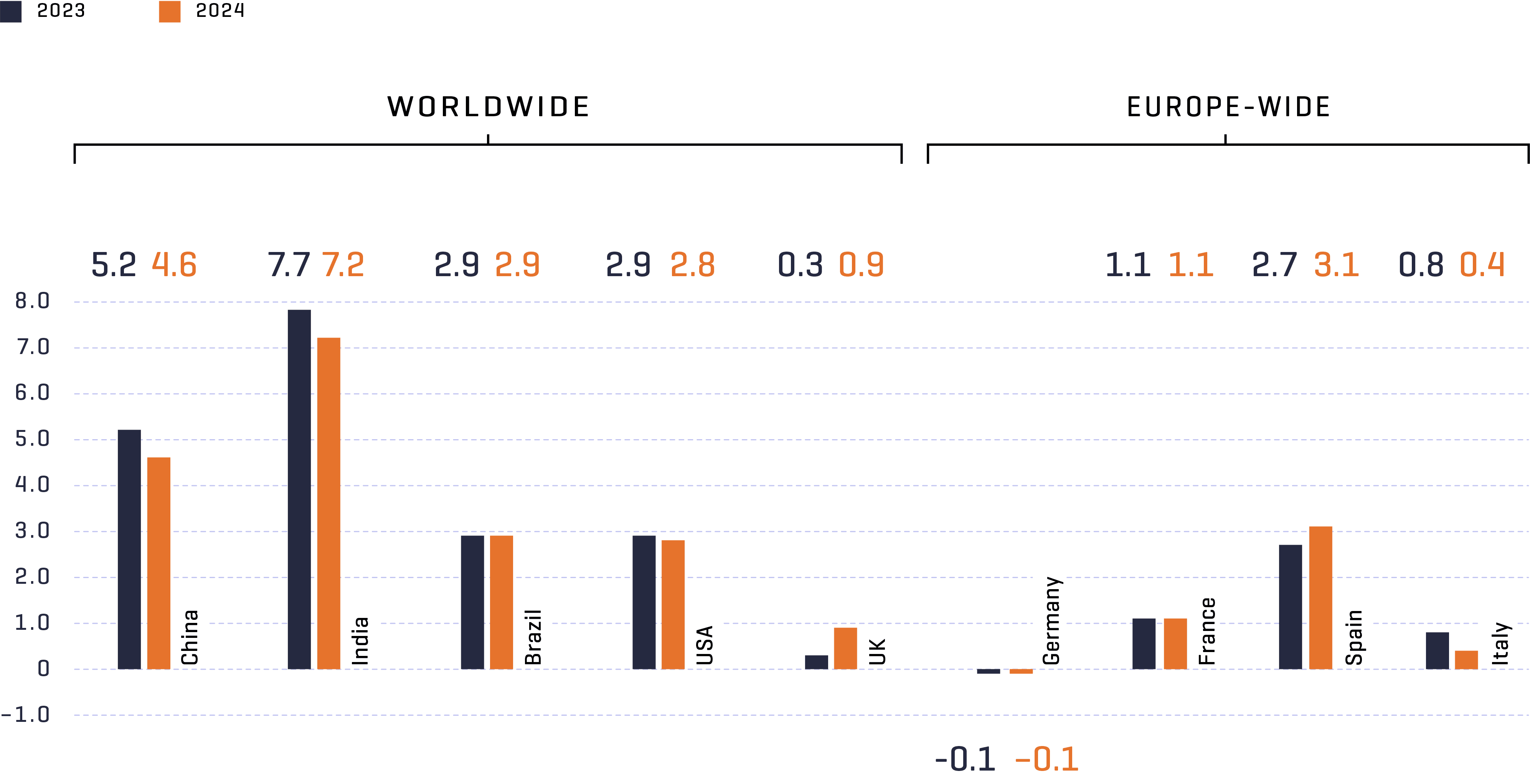

In 2024, the global economy was weighed down primarily by numerous geopolitical crises and continued restrictive monetary policies adopted by various national economies. The high levels of inflation of previous years in many parts of the world fell for the first time in 2024. Global economic growth was slightly below the long-term average. Nonetheless, global real gross domestic product (GDP) grew by 2.6% (2023: 2.9%), which was 0.6% higher than forecast3).

In the emerging markets, the economy grew at an overall rate of 4.4% (2023: 4.9%). The economy of the People’s Republic of China was negatively affected by the persistent real estate crisis and relatively weak domestic demand. Positive impetus came from the export industry. Overall, China’s GDP grew by 4.6% (2023: 5.2%). In the Asian region, it was mainly India that contributed to strong growth with GDP rising at a rate of 7.2% (2023: 7.7%).3)

The economies of the industrialized nations suffered especially from the restrictive monetary policy implemented to combat inflation. Despite the turnaround in interest rates instituted in the course of 2024, the impacts can still be clearly felt. Investment activity and private consumption were subdued. Overall, the leading economies recorded a weak 1.7% increase in GDP (2023: 1.8%). Positive stimuli were provided primarily by the US economy, where GDP grew by 2.8%. Private and public consumption, capital investments in equipment, and export performance all trended up here. The British economy grew significantly at a rate of 0.9% year-on-year (2023: 0.3%)3).

The economy in the euro zone grew by 0.7%. The growth was spread unevenly among the member states. While economic output in Spain and France developed in a positive direction, Germany lagged a significant distance behind. Industrial activity continued to weaken overall. The European Central Bank started to cut its key interest rates again in 2024 following substantial hikes in the previous years. The restrictive focus of monetary policy was maintained, however. The labor market in the euro zone proved to be robust. As a result, the unemployment rate was low based on a long-term comparison4).

Economic growth of selected countries

GDP growth 2023 and 20241) in %

ifo Institute, Economic Forecast Winter 2024, December 2024; German Council of Economic Experts, Annual Report 2024/25, November 2024

The German economy remained stuck in crisis in 2024. Structural changes, such as decarbonization, digitalization, demographic change, and deglobalization, forced companies to adjust their production structures. High energy, labor and regulatory costs reduced companies’ competitiveness. Unfavorable financing conditions put a brake on investment activity, especially in the industrial and construction sectors. The inflation rate fell sharply from the previous year (5.9%) and at 2.2% on average during the year was close to the target of 2.0%. Real wages also increased again as a result of higher wage agreements. Nevertheless, private consumption failed to recover as people continued to save (−0.1%). Foreign trade also declined because of the moderate global economic activity and the diminishing competitiveness of German companies. Imports and exports decreased by 0.1% and 0.6%, respectively. Compared to the previous year, the unemployment rate rose by 0.3 percentage points to 6.0%. Overall, Germany’s GDP shrank by 0.1% in 20243).

In 2024, the oil price (Brent) fluctuated in a range between USD 69 and USD 92 per barrel. The price reached its highest point in the middle of April and the lowest point on September 10. At the end of the year, the oil price was around USD74 per barrel.5)

Economic environment air traffic (Aviation)

Significant recovery in traffic

According to data from the International Air Transport Association (IATA), which is based on revenue passenger kilometers (RPK), global passenger traffic grew in 2024 by 10.4% compared with the previous year. The capacity utilization of aircraft climbed year-on-year to 84%. With an increase of 8.7%, the trend in Europe lagged behind the global performance. The growth driver was the Asian market, which grew by 16.9%6).

After the weakness in the year before, global freight volumes recovered again and grew by 11.3% measured by cargo tonne kilometers (CTK). At 11.2 %, demand in Europe grew by close to the same level. Asian freight traffic put in the strongest performance with growth of 14.5 %7).

Publications of the Airport Council International/Europe (ACI) trade association showed a stable Europe-wide recovery in passenger traffic of 7.4%. The pre-crisis level was thus exceeded by 1.8%. Germany, on the other hand, remained a significant 16% below the reference year of 2019 and thus recorded the worst recovery in the major European markets segment. On a positive note, Munich Airport ranked among the top-performing mega hubs with passenger growth of 12.2%. Factors such as the shortage of skilled labor, delays in aircraft deliveries, and geopolitical tensions are hampering even higher growth.8)

In its European Aviation Overview 2024, the European air traffic control service provider Eurocontrol analyzed the development of flights and flyovers in Europe while taking the pre-crisis levels into account. 96% of the traffic in the reference year of 2019 was reached in the period under review, corresponding to growth of 5% from the previous year. As Europe’s third-largest market, Germany recorded lower than average growth of 4% and remained a significant 16% below pre-crisis levels. As far as the airlines were concerned, Eurocontrol looked at the average number of flights a day. The Lufthansa Group was one of the worst performers here (+1% growth from the previous year and −23% down on the reference year of 2019). Strong recovery rates were recorded in particular by the low-cost providers Ryanair and Wizz Air with increases of +31% and +42% respectively from pre-crisis levels9).

The Bundesverband der deutschen Luftverkehrswirtschaft (BDL – German Aviation Association) warned in its report on the trends in German air traffic in 2024 of a dramatic loss of competitiveness. This development was reportedly triggered primarily by exorbitant state-induced location costs, which had reached a dangerous tipping point. For example, government location costs for handling an Airbus A320 in Frankfurt were 4,843 euros. In Istanbul, they were just 522 euros. In an international comparison, then, the development of traffic in Germany lagged a significant distance behind and achieved a recovery rate of only 85% of pre-crisis levels. In contrast, the rest of Europe was able to record a recovery rate of 104%. Germany thus occupied fourth last place out of 32 European countries. In part as a result of these locational disadvantages, the trend where traffic is shifting abroad continued, with hubs in Turkey or the Gulf and Chinese airlines in particular benefiting from this in the long-haul traffic segment10).

The airports organized in the Arbeitsgemeinschaft Deutscher Verkehrsflughäfen (ADV – German Airports Association) recorded significantly better traffic figures in 2024 than in the previous year. A total of 212.1 million airline passengers were processed (+7.5%). Aircraft movements grew in the comparison period by 3.0 % to around 1.8 million. At 4.8 million tonnes, cargo volume (airfreight and airmail throughput) recorded growth of 1.8%. Some Germany-wide traffic results were significantly below pre-crisis levels, however. In terms of passengers, 85% of the numbers recorded in 2019 were achieved, whereas aircraft movements were still 21% lower and cargo volume 0.4% lower11).

Economic environment Commercial Activities

Parking – dependence on passenger volume and passenger mix

Demand for parking rose in line with the higher volume of departing passengers, which is also reflected in the revenue. 58% of air passengers arrived on their own, which represents a slight increase over 2023. The high-revenue business traveler segment is still considerably smaller than it was in 2019. Most of this was successfully compensated by demand-oriented yield management.

Brick and mortar retail stagnates

As a result of high inflation, consumption saw only moderate year-on-year growth in 2024, rising 2.2% to 663.8 billion euros, equivalent to a real decrease of 0.9%, according to the Handelsverband Deutscher Einzelhändler (HDE – Association of German Retailers). The nominal growth was generated with a lower share accounted for by the brick and mortar retail segment (2024: +1.8%)12).

In December 2024, the business climate in the retail sector deteriorated slightly by 2.0 percentage points year-on-year13).

Gastronomy and hotel industry – revenue trending down

Compared to the previous year, revenue in the food and hotel sector saw only little growth of 0.6% nominally, which is equivalent to a 2.5% decline on a price-adjusted basis.14)

Some industry sectors experienced the following changes compared to the previous year: in the hotel and other accommodation sector, revenue grew by 2.6%, which is equivalent to a decline of 0.4% on a price-adjusted basis. The gastronomy sector recorded a 0.4% decline in revenue (−3.7% in real terms). Only the catering sector shows improved figures of 3.9% in nominal terms (real 0.0%)14).

Advertising business – strong growth in out of home advertising

Compared to the previous year, revenues generated by the Out of Home advertising category, which is relevant for the airport, increased by around 12.7% to reach 3.3 billion euros in Germany15).

Economic environment Real Estate

Munich office leasing market continues on path to recovery

The Munich office leasing market continued its upward trend at the end of the year, achieving take-up, including owner-occupied space, of 606,200 m² (2023: 474,800 m²). This is equivalent to a year-on-year increase of 27.7%. Excluding owner-occupied space, the purely rental performance was 551,600 m² (2023: 448,300 m²). Demand remains below average. Take-up was still around 20% lower than the long-term average.16)

Vacancy levels rose significantly again, as existing space that becomes available is frequently remaining unused for longer period and even new build space outside of central locations are often not yet leased on completion. As a result, vacancy levels exceeded the 2-million-m² mark (2023: 1.57 million m²), and the vacancy rate in the entire Munich market has also reached an all-time high at 8.7% (2023: 6.9%). In the central locations, the vacancy rate was 5.2% (2023: 3.5%), while in the other districts it stood at 11.1% (2023: 8.3%). The vacancy rate in the surrounding region rose from 9.5% to 10.5%.16)

Despite the increase in the supply of space, rents continued to trend upward. Average rent rose by 5.4% to € 25.10/m² (2023: € 23.80/m²), while prime rents even jumped 11% to € 53.50/m² (2023: € 48.20/m²). Lessees are thus preferring high-quality spaces, where incentives such as rent-free periods, relocation allowances or fit-out subsidies have continued to gain in importance, allowing lessees to make savings. In urban locations characterized by a highly competitive landscape, average rents in existing buildings barely increased, averaging € 29.10/m², as was already the case in the previous year.16)

There is currently just under 655,100 m² of office space under construction, 56% of which is already leased or earmarked for owner-occupied use. As things stand at the moment, 355,000 m² of this will be completed in 2025, with 71% already set to be occupied. A significant reduction in supply will be seen from 2026 onward, as this is when the existing caution shown by project developers since 2022 will become noticeable. It can be assumed that the increase in the vacancy rate will slow down, as not so much space will be added to the market.16)

The Munich office leasing market showed signs of recovery following the weak performance in the previous year. The sluggish economy will also mean only a below average take-up of space at the level of the past year will be achieved in 2025, with vacancy levels continuing to rise. This relates in particular to the important automotive industry in Munich. Other users from the manufacturing industries are still as active on the market as before, however, including technology companies from the aerospace and also the robotics sectors16).

Course of business

Key events in the past fiscal year

Strong upward trend and economic progress

In addition to the continuing increase in demand in the point-to-point traffic segment, passenger transfer traffic in particular provided substantially higher traffic figures in 2024. This had a positive impact on Munich Airport’s business figures, but also posed challenges for it at the same time: despite intensive and successful recruitment measures, it was not possible to reach the planned personnel resources in full, especially in the labor-intensive, operating divisions. Moreover, the parallel conversion to modern and more efficient security checkpoints had an adverse impact on operations.

Munich Airport consistently pursued its strategy of focusing on the core business of airport operations and its direct ancillary businesses and optimized the operational processes in cooperation with its partners.

Despite the challenges described above, strong growth in traffic volume was evident again in all areas in 2024. The impact of this meant that Munich Airport was the fastest growing airport in Germany in 2024.17)

Skytrax: 5-star awards for the airport and for Newark Airports Terminal A in New Jersey

The new Terminal A operated by a Munich Airport company at Newark Liberty International Airport was awarded five stars for the first time in March 2024 by Skytrax, the leading rating organization in the aviation industry. It has thus recorded the highest worldwide measurement of customer satisfaction at an airport terminal and is now part of a small, exclusive group of just three 5-star airport terminals in the whole of North America. With this accolade awarded to Terminal A in Newark, Munich Airport is the only operator of 5-star airport infrastructure on two different continents in the world.

Topping-out ceremony for the ibis Styles hotel at Munich Airport

April 2024 saw Munich Airport, the Accor Hotel Group, and various construction companies celebrate the topping-out ceremony for the new ibis Styles Munich Airport Hotel. Specific measures were implemented to be able to include the building in FMG’s sustainability strategy. The use of stone wool instead of rigid foam in the thermal insulation system, a green roof, geothermal cooling, and access to district heating powered by renewable energy sources all make a significant contribution to reducing the building’s carbon emissions.

Airport subsidiary expands to Hallbergmoos

The opening of O2 SURFTOWN MUC in Hallbergmoos in the summer of 2024, with around 220 places indoors and outdoors, marks the first time that Allresto, the FMG subsidiary in the gastronomy sector, has operated a restaurant outside of the airport campus. Great attention was paid in the design of the restaurant to ensure it is ideally integrated in the surrounding area and meets international standards.

Technical University of Munich becomes new tenant at LabCampus

With the Technical University of Munich (TUM) as a new tenant, the innovation campus covering around 500,000 m2 continues to be developed in the west of the airport grounds. International corporations, hidden champions, and start-ups encounter ideal conditions for collaboration on the LabCampus. This can be seen on site in the upcoming establishment of a «TUM Convergence Center» and the construction of the «TUM Sustainable and Future Aviation Centers». The aim here is to enable students, talented scientists, start-up teams, and business partners to develop viable, efficient, and more sustainable solutions through research focusing on aeronautics, mobility, robotics and security.

Aviation business

Two-digit passenger growth in 2024

Over the entire year of 2024, traffic trends were at times well above the previous year’s result. However, the values of the pre-crisis period were not reached.

Traffic figures Munich Airport1)

Change | ||||

|---|---|---|---|---|

2024 | 2023 | Absolute | Relative in % | |

Aircraft movements | 327,228 | 302,150 | 25,078 | 8.3 |

Passengers (in millions) | 41.6 | 37.0 | 4.6 | 12.2 |

Airfreight throughput (in tonnes) | 307,635 | 277,199 | 30,436 | 11.0 |

Airmail throughput (in tonnes) | 3,455 | 7,147 | −3,692 | −51.7 |

deviations possible due to rounding

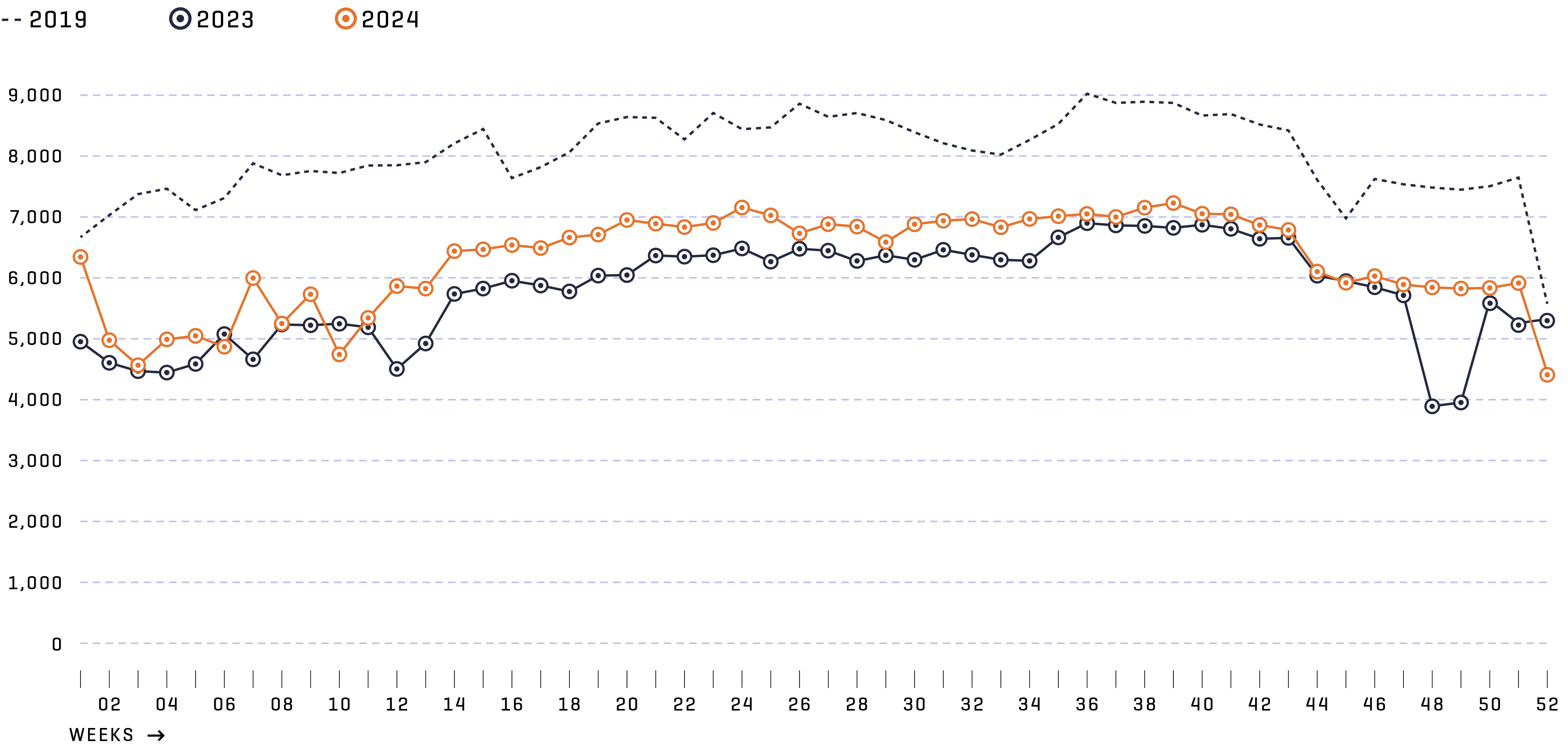

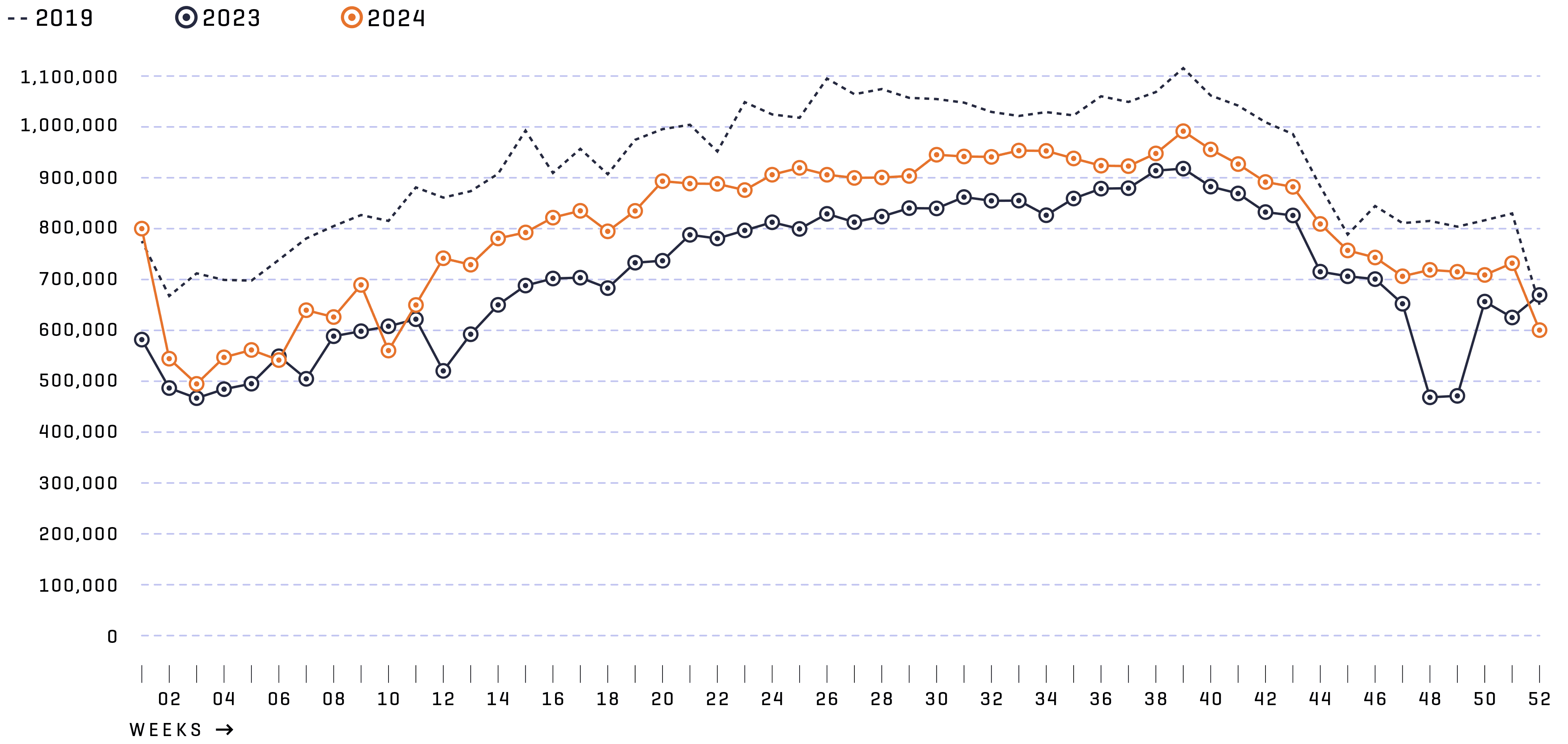

With 41.6 million airline passengers (+12.2%) and 327,228 aircraft movements (+8.3%), traffic figures at Munich Airport increased markedly over the previous year. Still, passenger figures and movements were only 87% and 78% of the values in the 2019 reference year, respectively.

Munich Airport started out from a high level in 2024. An ongoing recovery trend was already noticeable during the Easter holidays and continued to gain traction from Whitsun onward. As in the previous year, very high utilization rates (82%) and high ticket prices show that it was sometimes difficult to meet demand.

Aircraft movements at Munich Airport during the year

Aircraft movements in thousands by calendar week 2019/2023/2024 (commercial traffic)

The worldwide lifting of travel restrictions led to a significant recovery in long-haul traffic. The number of connections to some destinations such as the USA were already higher in the previous year than in the comparison period of 2019. The important Asian market presented a mixed picture. Because of the delay in re-opening the market and constraints in personnel and aircraft, China continued to lag behind, while smaller markets such as India and Thailand surpassed the levels seen before the crisis. In 2024, a good 8.2 million commercial passengers were transported in the long-haul segment, an increase of 17% over 2023, but 3% lower in comparison with 2019.

Just under 6.2 million commercial travelers were conveyed within Germany in 2024, which was 7% higher compared to the previous year, but 36% lower compared to 2019. German traffic continued to recover over the course of the year, which, in view of high ticket prices, was primarily attributable to growing demand in the business travel segment.

Continental traffic also saw a significant recovery. Approximately 27.2 million commercial airline passengers used Munich Airport, which equated to an increase of 12%. At the same time, however, passenger volumes were still around −9% lower than in the 2019 reference year. Capacity utilization reached a new record of 82% across all segments with an 11% increase in seats available. The hub traffic of Deutsche Lufthansa, which accounted for a strong 42% of connecting passengers, was an important reason behind this development (2023: 41%; 2019: 39%).

Passenger development at Munich Airport during the year

Passengers by calendar week 2019/2023/2024 (commercial traffic)

Similarly, commercial airfreight throughput also improved by 11% over the previous year to reach 307,635 tonnes, which was only 7% below the pre-crisis level. As the long-haul passenger segment continued to recover, bellyhold cargo volumes handled in Munich increased by 26 % compared to 2023 to reach 272,707 tonnes (−5% compared to 2019). The share of bellyhold cargo out of the total freight volume increased to 89%, which thus exceeded the level of a good 80 % normally seen before the crisis. Generally speaking, the demand for airfreight stabilized globally during the period under review.

Airfreight throughput decreased to approximately 3,455 tonnes (−51.7%) and was thus only around 19% of the 2019 volume.

Compared to the airports organized in the ADV, Munich Airport saw above-average growth in all segments. Frankfurt Airport, last year’s growth driver, experienced only subdued growth, while catch-up effects were seen in Munich. A noteworthy feature in the airfreight segment was that the major freight-only locations of Hahn, Cologne/Bonn, and Leipzig/Halle saw negative trends.

Traffic in 20241)

in %

ADV | Munich | |

|---|---|---|

Movements (total traffic excluding non commercial traffic) | +3.0 | +8.3 |

Airline passengers (commercial traffic) | +7.5 | +12.2 |

Cargo (airfreight and airmail including transit) | +1.9 | +9.4 |

ADV, ADV-12.2024_MoSta-Flughäfen

The ranking of European airports with the highest traffic volumes has been characterized by extreme changes since the start of the pandemic and an incomplete data situation and is also being influenced by the impacts of the Russian attack on Ukraine. Measured by passenger volume and aircraft movements, Munich holds 10th and 9th place respectively in the ranking of European airports with the highest traffic volumes. Despite the positive local traffic trends, Munich fell back in a Europe-wide comparison. This can be attributed mainly to the general political situation and in particular the extremely high government-induced location costs18).

Ground handling services in a difficult economic and operating environment despite recovery

The subsidiary AE Munich increased handling numbers substantially in 2024. This was primarily due to the further recovery in air traffic and the takeover of handling contracts from the subcontractor of the previous second license holder Swissport-Losch (SPL) for aircraft and baggage handling.

There are two ground handling licenses at Munich Airport. One of these is permanently assigned to AE Munich. The previous owner of the second license, SPL, lost it with effect from March 1, 2024 and thus also the ground handling contracts that it had previously entered into with the various airlines.

Fears of high staff turnover arose at SPL following the loss of the ground handling license. Together with the already strained personnel situation in ground handling services, this would have led to increased risks for the performance of the ground handling services in the summer of 2024. To minimize the risks at Munich Airport, an agreement was entered into with SPL engaging the company as a subcontractor with effect from March 1, 2024, to service the corresponding contracts taken over from the airlines.

Market share increased by 32.1% to reach an average of 93.5% in 2024 essentially as a result of the subcontractor engagement.

Commercial Activities business

Revenue in the Commercial Activities business unit grew by 12.2% compared to the previous year, partly as a result of the increase in passenger volumes.

Parking – revenue exceeds pre-crisis level

In 2024, revenue in the area of parking and mobility grew positively at +13% year-on-year, a rate that was disproportionate to the volume of origin and destination/O&D passengers. Revenue that was 14% higher compared to the pre-crisis level in 2019 was achieved for the first time in 2024. The equates to a significantly above-average revenue performance in view of the O&D passenger figures that are still −18% down when compared with the pre-crisis level in 2019.

As renovations continue and parking spaces are consequently unavailable, the capacity situation remains strained particularly in the central zone.

The rental car business performed well in line with passenger figures. The fall in prices for rental cars continued, as the shortage of vehicles that had previously driven prices up was resolved. Here, too, there continued to be challenges caused by capacity constraints and the first indications of resulting limits to growth. Significant growth was achieved in the area of tenant parking, which is independent of passengers, thanks to special effects and another price rise. Car sharing was also an element of this at Munich Airport.

Retail – revenue growth disproportionate to passenger developments

Revenue in the retail segment rose by 17% year-on-year. Revenue per passenger increased by 4%. A particular contribution to this growth came from the strong consumer behavior during the major concert events that were held in Munich and the Euros (the European Football Championship), which were hosted by Germany. Munich Airport continues to see only small numbers of wealthy international travelers from destinations such as China, Russia and the Ukraine, however.

Gastronomy – revenue per passenger declines

Compared with the previous year, sales in the restaurants and bars rose by 8% in nominal terms. This growth was considerably higher than the market trend of −0.4%. The reason for this performance can be attributed to the 12% growth in passenger volumes. Revenue per passenger declined slightly by 3%, however.

The 5-star hotel in the central area of Munich Airport recorded an increase in revenue and occupancy rates – also thanks to the effects of the major concerts and the Euros. It was named the best airport hotel in Europe again at the Skytrax Awards 2024, after being ranked second the previous year19).

Advertising – strong performance in line with the market environment

Advertising revenue at the airport rose by 14%, a rate slightly higher than the industry trend. Here, too, strong bookings during the Euros and also during fairs were the key factors.

Real Estate course of business

Ongoing site and real estate development

Munich Airport is currently building another hotel (ibis Styles) on the parcel of land that borders Novotel to the south. Its construction, which comprised the interior work and the facade in 2024, continues to progress. The hotel is expected to start operations by the first quarter of 2026 at the latest.

Progress was successfully made on the construction work for the new pier that is set to expand Terminal 1, especially on the interior construction. The first tenants of the future market place also started their interior fit-out works toward the end of 2024. The district heating connection for the terminal extension was also put into operation.

New parking capacity has been available since February 2024 when P43 was completed. Construction of the new P8 also began in May 2024. A total of 3,650 parking spaces will be created here, 20% of which will be set up for e-mobility. It is expected that the parking garage will be completed at the end of 2026.

TUM was won over as a tenant for the LabCampus site when a long-term lease was entered into in October 2024. The university will move in in 2025. The TUM Convergence Center will be established and additionally the TUM Sustainable and Future Aviation Center will be set up on around 20,400 m² of the LabCampus, the innovation hub at Munich Airport. Moreover, approximately 3,000 m² was handed over to two new tenants in the course of the year. This means that LAB 52 is now fully leased, while 25%, or 7,000 m², of the space in LAB 48 is still available.

Results of operations, assets, and financial position

Results of operations

Earnings after taxes – continuing the growth trajectory

In the 2024 fiscal year, Munich Airport’s earnings after taxes (EAT) improved significantly by TEUR 39,026 to TEUR 64,374. The various developments are explained in detail below.

Results of operations

in TEUR

Change | ||||

|---|---|---|---|---|

2024 | 2023 | Absolute | Relative in % | |

Revenue | 1,621,405 | 1,373,301 | 248,104 | 18.1 |

Other income | 39,685 | 43,201 | −3,516 | −8.1 |

Total revenue | 1,661,090 | 1,416,502 | 244,588 | 17.3 |

Cost of materials | −542,974 | −461,641 | −81,333 | 17.6 |

Personnel expenses | −596,873 | −541,586 | −55,287 | 10.2 |

Other expenses | −123,148 | −95,614 | −27,534 | 28.8 |

EBITDA | 398,095 | 317,661 | 80,434 | 25.3 |

Depreciation and amortization | −203,161 | −202,790 | −371 | 0.2 |

EBIT | 194,934 | 114,871 | 80,063 | 69.7 |

Interest result | −83,367 | −97,001 | 13,634 | −14.1 |

Other financial result | −10,265 | 21,106 | −31,371 | >100.0 |

Result from investments | 1,797 | 1,287 | 510 | 39.6 |

Financial result1) | −91,835 | −74,608 | −17,227 | 23.1 |

EBT | 103,099 | 40,263 | 62,836 | >100.0 |

Income taxes | −38,725 | −14,915 | −23,810 | >100.0 |

EAT | 64,374 | 25,348 | 39,026 | >100.0 |

This also includes the results from companies accounted for using the equity method.

The noticeable recovery in traffic in 2024, especially in continental and intercontinental traffic, led to an increase in revenue from airport charges from TEUR 516,363 to TEUR 621,572 (+20.4%). Nevertheless, revenues remained slightly below the pre-crisis year of 2019.

Revenue from ground handling services also increased by a total of TEUR 77,412 to TEUR 226,591 due to the increase in flight movements and passenger numbers as well as the takeover of the ground handling service contracts from SPL on 1 March 2024.

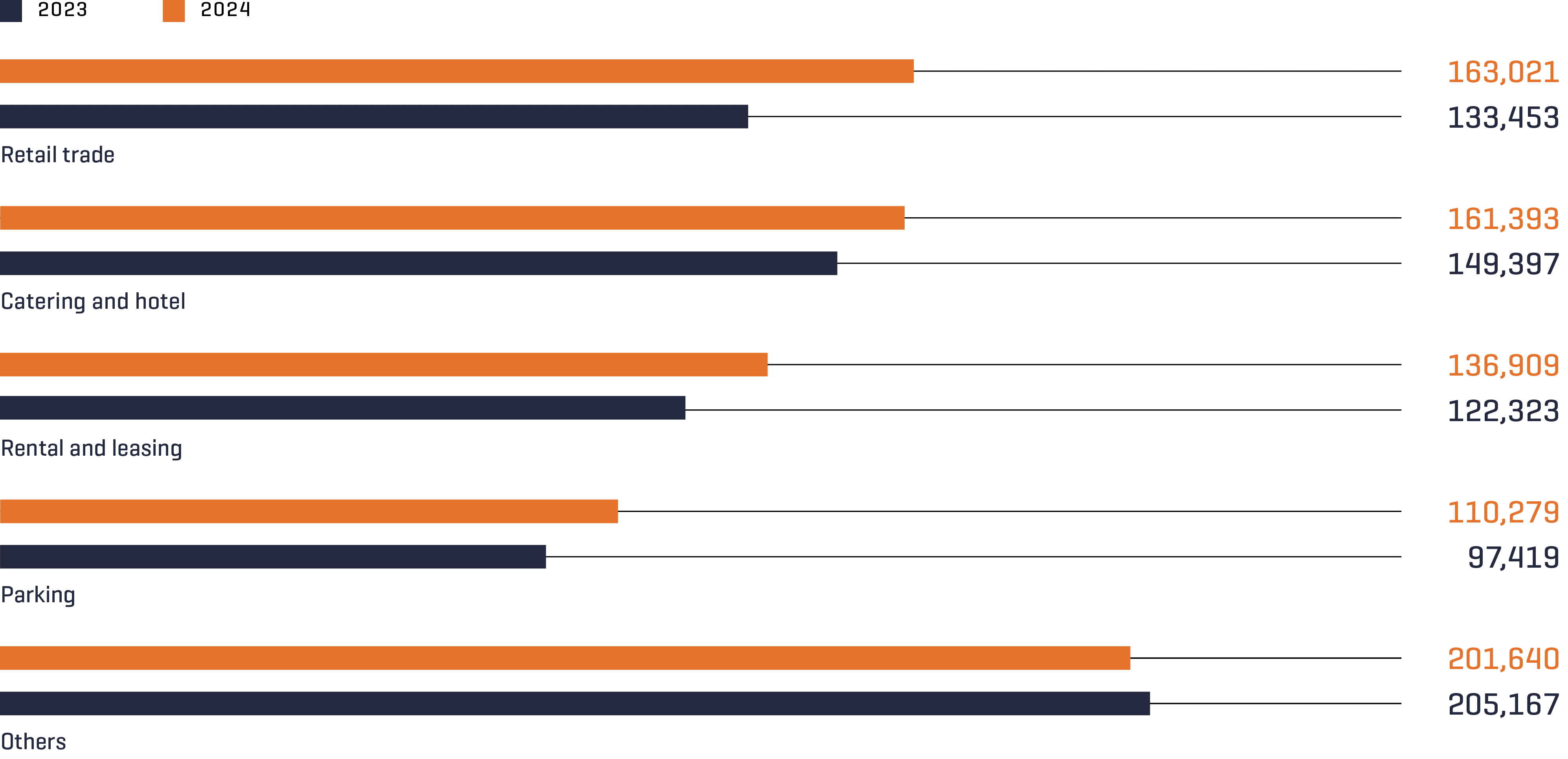

Revenue in the other divisions developed as follows:

Breakdown of revenue

in TEUR

Comparing the revenue in 2024 with the revenue in the pre-crisis year of 2019, only the revenue from the retail trade is still lower than the figures recorded in 2019, which can be attributed to the absence of wealthy international passengers from destinations such as China, Russia, and Ukraine.

Other revenues include global management, consulting and training services for the aviation industry, as well as utility services and fuel.

After more than 30 years of operation, the need for renovation of the buildings from the first expansion phase of Munich Airport continues to grow. Accordingly, expenses for refurbishment, optimization, and conversion measures increased by TEUR 9,726 to TEUR 138,682. The remaining items in the cost of materials increased mainly as a result of the significant increase in air traffic. Overall, the cost of materials increased by TEUR 81,333 (17.6%).

Personnel expenses at Munich Airport increased by 10.2% to TEUR 596,873 as a result of collectively agreed pay rises, effects from the industry-wide collective agreement for ground handling services, and numerous measures to provide employees with financial support. In addition, the number of employees grew significantly from 8,193 to 8,821 people on average, which was the result of a large-scale recruitment program implemented to ensure operations.

At TEUR 123,14, other expenses were a considerable 28.8% higher than the previous year’s level. Major reasons for the rise were higher rental and lease expenses, audit, consulting, and project costs, and expenses arising from the recruitment program for new employees in ground handling services (including for language training courses and agency fees).

The financial result, including the result from companies measured using the equity method deteriorated by TEUR 17,227 to TEUR −91,835, where this was caused primarily by the increase in interest expenses on loans and the remeasurement of the financial liabilities from interests in partnerships.

Expenses related to income taxes are due to the positive results generated in the Group.

Assets and financial position

Assets – Liquidity continues to be guaranteed

Financial position

in TEUR

Change | ||||

|---|---|---|---|---|

As of Dec. 31, 2024 | As of Dec. 31, 2023 | Absolute | Relative in % | |

Non current assets | 5,379,804 | 5,272,539 | 107,265 | 2.0 |

Current assets1) | 229,944 | 407,057 | −177,113 | −43.5 |

thereof cash and cash equivalents | 8,756 | 11,201 | −2,445 | −21.8 |

Assets | 5,609,748 | 5,679,596 | −69,848 | −1.2 |

Equity | 1,851,140 | 1,786,679 | 64,461 | 3.6 |

Other non current liabilities2) | 2,813,167 | 2,636,230 | 176,937 | 6.7 |

Other current liabilities2) | 945,441 | 1,256,687 | −311,246 | −24.8 |

Equity and liabilities | 5,609,748 | 5,679,596 | −69,848 | −1.2 |

including assets held for sale

including financial liabilities from partnerships and liabilities from the intention to sell

The increase in non current assets (TEUR +107,265) related primarily to the property, plant and equipment for own use, which totaled TEUR 99,291. As a result of several building projects, such as the expansion of Terminal 1 and the construction of the ibis Styles hotel, advance payments and assets under construction increased by a total of TEUR 193,138 to TEUR 676,280. Investments in property, plant and equipment for own use at Munich Airport totaled TEUR 297,812 in 2024. These were offset by depreciation of TEUR 193,815.

The significant decline in current assets (TEUR −177,113) resulted essentially from the fall in liquidity reserves as at the end of the reporting period (TEUR −187,964) to TEUR 13,477. These were used in 2024 primarily to repay the loans to shareholders in the amount of TEUR 250,000.

The increase in equity to TEUR 1,851,140 can mainly be attributed to the group profit for the current 2024 fiscal year of TEUR 64,374.

The changes in other liabilities can essentially be assigned to the financing division. The decline can primarily be attributed to repayments of loans or loans to shareholders. Conversely, financial liabilities from interests in partnerships increased by TEUR 32,465. Other repayments of loans or loans to shareholders fall due in 2025.

Capital structure

in TEUR

Change | ||||

|---|---|---|---|---|

As of Dec. 31, 2024 | As of Dec. 31, 2023 | Absolute | Relative in % | |

Subscribed capital | 306,776 | 306,776 | – | – |

Reserves | 163,161 | 131,610 | 31,551 | 24.0 |

Other equity | 1,381,182 | 1,348,273 | 32,909 | 2.4 |

thereof profit/loss of the year | 64,374 | 25,348 | 39,026 | >100.0 |

Non controlling interests | 21 | 20 | 1 | 5.0 |

Equity | 1,851,140 | 1,786,679 | 64,461 | 3.6 |

Financial liabilities from interests in partnerships | 431,245 | 398,780 | 32,465 | 8.1 |

Shareholder loans1) | 257,749 | 518,315 | −260,566 | −50.3 |

Fixed-rate loans | 1,866,277 | 1,794,820 | 71,457 | 4.0 |

Floating-rate loans | 408,628 | 465,809 | −57,181 | −12.3 |

Loans | 2,274,905 | 2,260,629 | 14,276 | 0.6 |

Derivatives | 3,018 | 1,920 | 1,098 | 57.2 |

Other liabilities | 791,691 | 713,273 | 78,418 | 11.0 |

Financial liabilities | 3,758,608 | 3,892,917 | −134,309 | −3.5 |

Equity ratio | 33.0% | 31.5% | ||

including interest

The equity ratio increased significantly by 1.5% to 33.0% on account of the result for the 2024 fiscal year.

The main terms of Munich Airport’s current and non current financial liabilities can be found in the table below:

Terms for current and non current loans

as of December 31, 2024

Method of funding | Currency | Interest rate | Residual debt in TEUR | Interest rate in % | |

|---|---|---|---|---|---|

from | to | ||||

Financial liabilities from interests in partnerships | EUR | Earnings-based | 431,245 | – | – |

Shareholder loans | EUR | variable/earnings-based | 241,913 | Base rate plus margin | |

Loans | EUR | Floating-rate | 408,286 | 3M- and 6M-EURIBOR plus margin | |

Loans | EUR/USD | Fixed-rate | 1,723,921 | 0.16 | 5.95 |

The shareholder loans are due for repayment in the next fiscal year and bear interest at the prime rate plus a margin.

The loans have a final due date of 2025 to 2033.

The loans are subject to the usual non financial covenants, including pari passu declarations. In addition, there are other general conventional agreements concerning repayment in the event of changes in the shareholder structure. No financial covenants have been agreed.

In addition, unutilized credit lines as well as overdrafts and money market lines totaling TEUR 318,716 are available as of December 31, 2024.

Munich Airport counters risks from interest rate and exchange rate fluctuations by hedging with interest rate payer swaps and forward exchange transactions. The interest rate hedges are recognized as hedging relationships.

Liquidity

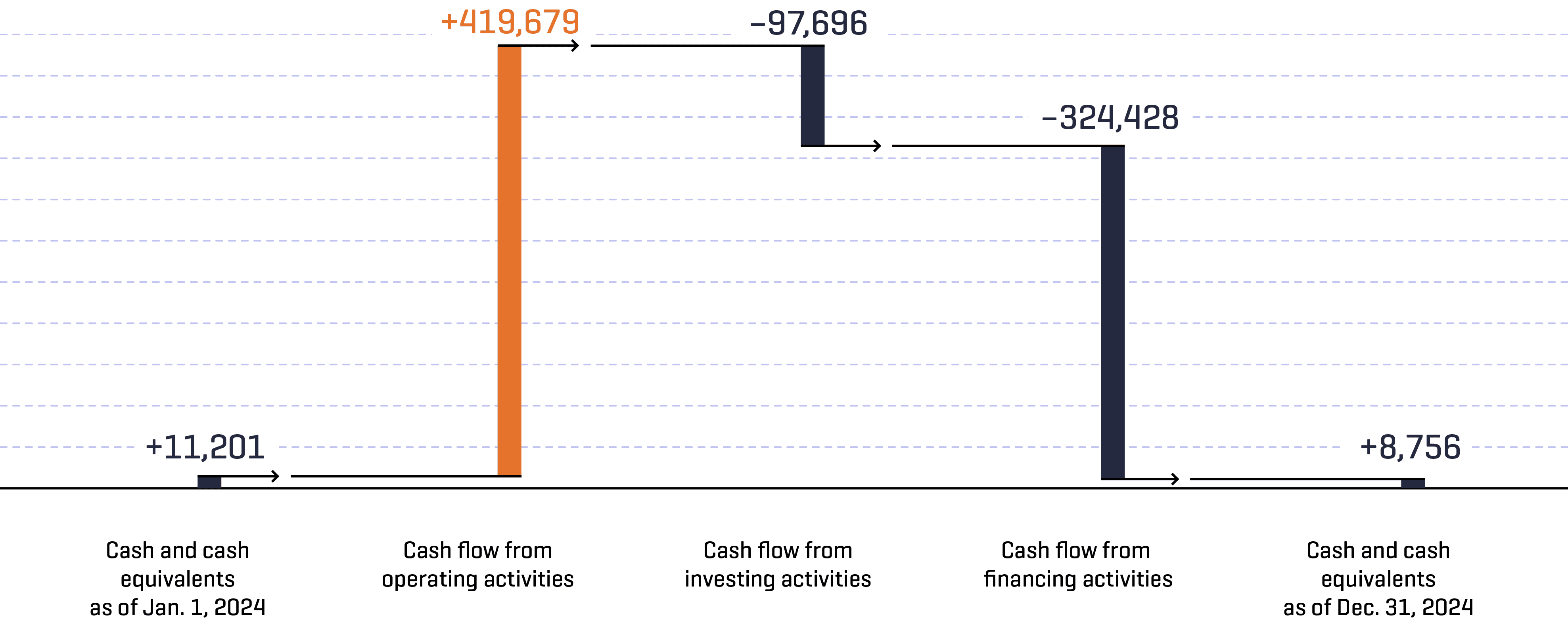

Statement of cash flows

in TEUR

Sufficient cash and cash equivalents were available from the cash flow from operating activities in 2024 to ensure the company’s liquidity in the business operations. Due to improved traffic developments and strict cost management, the cash flow from operating activities grew significantly in 2024 (previous year: TEUR +301,545).

Cash outflows from investing activities resulted primarily from the acquisition and production of property, plant and equipment and from the various construction projects, such as the expansion of Terminal 1.

Cash outflows from financing activities resulted primarily from the fact that loan repayments were higher than drawdowns. These payments were hedged at all times and were also successfully compensated again for the first time through the very high cash flow from operating activities. The Group reported cash flow from financing activities totaling TEUR 31,560 in the previous year.

Target achievement and overall assessment

Year on year and in comparison with the forecast development, the performance indicators have trended as follows:

Earnings before taxes (EBT)

Munich Airport’s EBT for the 2024 fiscal year significantly exceeded the planned figure. This was mainly thanks to the substantial recovery in traffic volume and the accompanying increase in revenue in all divisions.

Munich Airport thus generated positive earnings before taxes, as in the previous year.

Carbon reductions

Binding targets are defined annually in order to achieve the long-term climate protection goals. They include stipulations regarding the implementation and recognition of efficiency measures as well as special targets for the development of carbon-reduction technologies.

As in the previous year, the largest electricity savings, of approximately 2.5 GWh, were generated from the lighting systems, both in the indoor and outdoor areas. Following in second place were the ventilation and air conditioning systems, where savings of approximately 1.8 GWh were realized. Savings of approximately 0.6 GWh in heating and of approximately 0.2 GWh in cooling were also produced from ventilation and air conditioning technology. The continued electrification of the vehicle fleet brought an additional saving of 825 tonnes of CO₂.

Compared to the previous year, the emission factor used for electricity in accordance with the German Environment Agency (UBA) rose by approximately 5.5% (2023: +15%) to 459 g/kWh (2023: 435 g/kWh). This translates into greater carbon reductions than in the previous year from the same volume of energy saved.

Munich Airport had set itself the goal of saving 2,160 tonnes of CO₂ in 2024. The efficiency measures that were completed in 2024 produced savings of 3,047 tonnes of CO₂, thus exceeding the target that was set.

Passenger Experience Index (PEI)

Munich Airport recorded a considerable increase in passenger satisfaction as measured by the PEI in 2024. This can be attributed in particular to the ongoing optimization of passenger processes at the Munich site.

In order to meet the requirements of a 5-star airport, Munich Airport once again implemented measures to improve the passenger experience in 2024. For example, additional self-service bag drop units were installed in Terminal 1, the security checkpoints in Terminal 2 were upgraded to accommodate new CT scanners, and new SmartGates were installed to optimize central passenger flow through the security checks in Terminal 2. Other examples include the launch of new digital services («gaming» entertainment offer for arriving travelers), a snack robot, the upgrading and redesign of gastronomy and retail premises, and the introduction of services targeted at specific groups, such as new rental strollers for small children.

Lost Time Incident Frequency (LTIF)

In 2024, the LTIF for FMG and AE Munich was 14.3, which greatly exceeded the forecast value of 17.8, and was reduced by 11% from the 2023 figure. This decline is due to the slight reduction in occupational accidents (−1%) accompanied by a sharp increase in hours worked at the same time (+10%). A comparison of the LTIF for 2024 and 2019 (21.67) – before the outbreak of the Covid-19 pandemic – reveals a sharp decrease in incident frequency.

ifo Institute, Economic Forecast Winter 2024, December 2024; German Council of Economic Experts, Annual Report 2024/25, November 2024

German Council of Economic Experts, Annual Report 2024/25, November 24

IATA, Air Passenger Market Analysis, December 2024 /Different calculation of capacity utilization according to airline standard, seat kilometer sold/seat kilometer offered leads to higher values, no comparability with seat capacity utilization (airport method).

IATA, Air Cargo Market Analysis, December 2024

ACI Europe, press release of February 12, 2025

Eurocontrol, European Aviation Overview 2024, January 23, 2025

BDL, press release, Annual figures 2024, February 13, 2025

ADV, MoSta-Flughäfen (Monthly Traffic Report – Airports), December 2024

HDE, Annual Press Conference 2025, January 31, 2025

ifo Institute, Business Climate Index for Germany, December 17, 2024

Federal Statistical Office, press release no. 26 of January 21, 2025

Fachverband Außenwerbung e.V. (Out of Home Advertising Association), press release «Out of Home Balance

Sheet» of January 20, 2025

Colliers, press release «Münchner Bürovermietungsmarkt weiter auf Erholungskurs» («Munich office letting

market continues on path to recovery») of January 9, 2025

ADV, ADV-12.2024_MoSta-Flughäfen

ACI, Munich Airport Ranking 2024

SKYTRAX, World’s Best Airport Hotels 2024, November 2024